tax benefit rule state tax refund

When the couple paid the excess refund 400 to the state in the prior year it increased their itemized deduction on their federal return to 14000 from 13600. Allison received a state tax refund of 2300.

Say No To Cash Transaction In 2021 Cash Prevention Accounting

The most common situation would be that you deducted your state and local income taxes on your 2018 return and then received a state tax refund during the calendar year 2019.

. Tax Benefit Rule Of 111 Should Shield State Tax Refunds For Taxpayers Over The Salt Limit Current Federal Tax Developments Lime. An alternative fact pattern illustrates how a portion of the state income tax refund might be taxable. This means that the maximum taxable amount of any state refund that Allison received during 2019 is 6500 18500 less 12000The excess of what Allison paid in state and local income taxes over sales taxes in Allisons state is 4000.

Remember state refunds arent taxable if you itemized and if you opted to deduct state and local sales tax instead of state income tax. WASHINGTON The Internal Revenue Service today clarified the tax treatment of state and local tax refunds arising from any year in which the new limit on the state and local tax SALT deduction is in effect. Equivalently stated taxpayers must include in income any amounts recovered if they received a tax benefit in a prior year for that loss.

Apply the tax benefit rule to determine the amount of the state income tax refund included in gross income in 2021. The rule says if a refund can be linked to a prior deduction which the taxpayer actually benefitted from then the refund is taxable to the extent of that benefit. In Revenue Ruling 2019-11 PDF posted today on IRSgov the IRS provided four examples illustrating how the long-standing tax benefit rule interacts with the.

If the couple received a state tax refund of 500 in the current year the taxpayer will include all of the refund in their current year income. If you receive a refund of all or part of a deduction you claimed for example a state tax refund you must report as income the amount of tax benefit you had received from the amount of the refund. If a state or local income tax refund is received during the tax year the refund must generally be included in income if the taxpayer deducted the tax in an earlier year.

If a trust was limited to a 10000 state tax deduction in 2018 why should it then report the refund as income in 2019. As the Tax Court explained under the tax benefit rule as it applies to state income tax refunds for a taxpayer to be able to exclude a state income tax refund payment from income the refund payment must be for an overpayment of tax for which the taxpayer did not take a federal tax deduction when it was paid in a preceding year. 1500 refund of state income taxes paid in 2018.

Her itemized deductions totaled 18500 in 2018. There are other kinds of recovery items but the most common is a state tax refund. Had A paid only the proper amount of state income tax in 2018 As state and local tax deduction would have been reduced from 9000 to 7500 and as a result As itemized deductions would have been reduced from 14000 to 12500 a difference of 1500.

Their AGI was 85000 and itemized deductions were 25100 which included 7000 in state income tax and no other state or local taxes. Thus the 2000 refund is excluded from their 2019 income due to the operation of IRC 111. One common source that is frequently overlooked by tax advisors and more often misunderstood is the application of the tax benefit rule IRC section 111 to state and local tax refunds.

Your refund isnt taxable if the box there is checked. As such the amount of their state income tax refund provided no income tax benefit in 2018. Under the so-called tax benefit rule a taxpayer need not include in his gross income and therefore need not pay tax on it amounts recovered for his loss if he did not receive a tax benefit for the loss in a prior year.

Whether state refunds are includable on a federal return depends on the tax benefit rule. Now you must determine if you deducted sales taxes or income taxes. March 01 2019 by Ed Zollars CPA.

Copyright 2008 HR Block. In applying the AMT nonrefundable credits tax benefit rule to state income tax refunds the program assumes that if there was any tax benefit received in 20XX by deducting the entire amount of state income taxes refunded then the full amount of the refund after accounting for other adjustments is taxable. A state income tax refund is a recovery item whose taxability on your federal return is governed by the tax benefit rule of Internal Revenue Code section 111.

A state tax refund is taxable income if you received a tax benefit by deducting your state income taxes on a previous tax return. State tax refunds are only SOMETIMES taxable on the 1040. Their AGI was 92325 and itemized deductions were 27400 which included 6850 in state income tax and no other state or local taxes.

Why doesnt the 1041 program consider the tax benefit rule for state tax refunds. Basically the rule are set such that you cant game the system by taking a big deduction on state taxes overpaid in year 1 and then get the money refunded to you in year 2. The entire amount recovered in the current year had given the taxpayer a tax benefit.

A received a tax benefit from. This week a number of questions arose in different online tax discussion forums regarding the potential taxability of a state income tax refund for taxpayers where the taxpayers had their state tax deductions limited by the 10000. A rule that provides that the amount of an expense recovered must be included in income in the year of the recovery to the extent the original expense resulted in a tax benefit.

Look at line 5a of your previous years Schedule A. If an amount is zero enter 0. Tax Benefit Rule of 111 Should Shield State Tax Refunds For Taxpayers Over the SALT Limit.

State Local Tax SALT In Rev. Apply the tax benefit rule to determine the amount of the state income tax refund included in gross income in 2020. If an amount is zero enter 0.

However under the tax benefit rule the taxpayer must only include the refund up to the amount by which the deduction taken for the refunded amount reduced tax in the earlier year. Assume the same facts except their state tax refund was 5000. Tax benefit rule state tax refund Wednesday March 2 2022 Edit.

Myrna and Geoffrey filed a joint tax return in 2019. Myrna and Geoffrey filed a joint tax return in 2020. 2019-11 issued Friday the IRS addressed how the long-standing tax benefit rule interacts with the new 10000 limit on deductions of state and local taxes to determine the portion of any state or local tax refund that must be included on the taxpayers federal income tax return.

The most common example is a state income tax refund of tax deducted in the prior year. In year 2 your income is increased such that you eventually get taxed and the gimmick fails. Ad File 1040ez Free today for a faster refund.

Simply stated the refunds recoveries are taxable only to the extent the taxpayer received a tax benefit from the deductionthat is the deduction must have reduced taxes or.

S Corp Profitable Business Small Business Tips Tax Services

House Property Income Tax Refund

Budgeting 101 Tip Budgeting Money Saving Tips Budgeting 101

Taxpayers Can Choose To Itemize Or Take Standard Deduction For Tax Year 2017 Standard Deduction Deduction Income Tax

How Is E Filing Of Itr Done In India Filing Taxes Income Tax Tax Return

6 Benefits Of Filing Income Tax Return

Year End Planning Tips By The Numbers The Closing Quarter Of The Year Is A Great Time To Review You Relationship Management Investment Portfolio How To Apply

Things To Consider During This Tax Season Heights 406 969 2760 West End 406 894 2050 Taxes Payroll Bookkeeping Tax Refund Emergency Fund Investing

If You Are Stuck And Don T Know How To Claim Your Money Back From Irs No Need To Worry Feel Free To Contact Me For Tax Refund Bookkeeping Coaching Business

5 Ways A Tax Accountant Can Help Small Businesses Infographic Tax Accountant Small Business Infographic Accounting

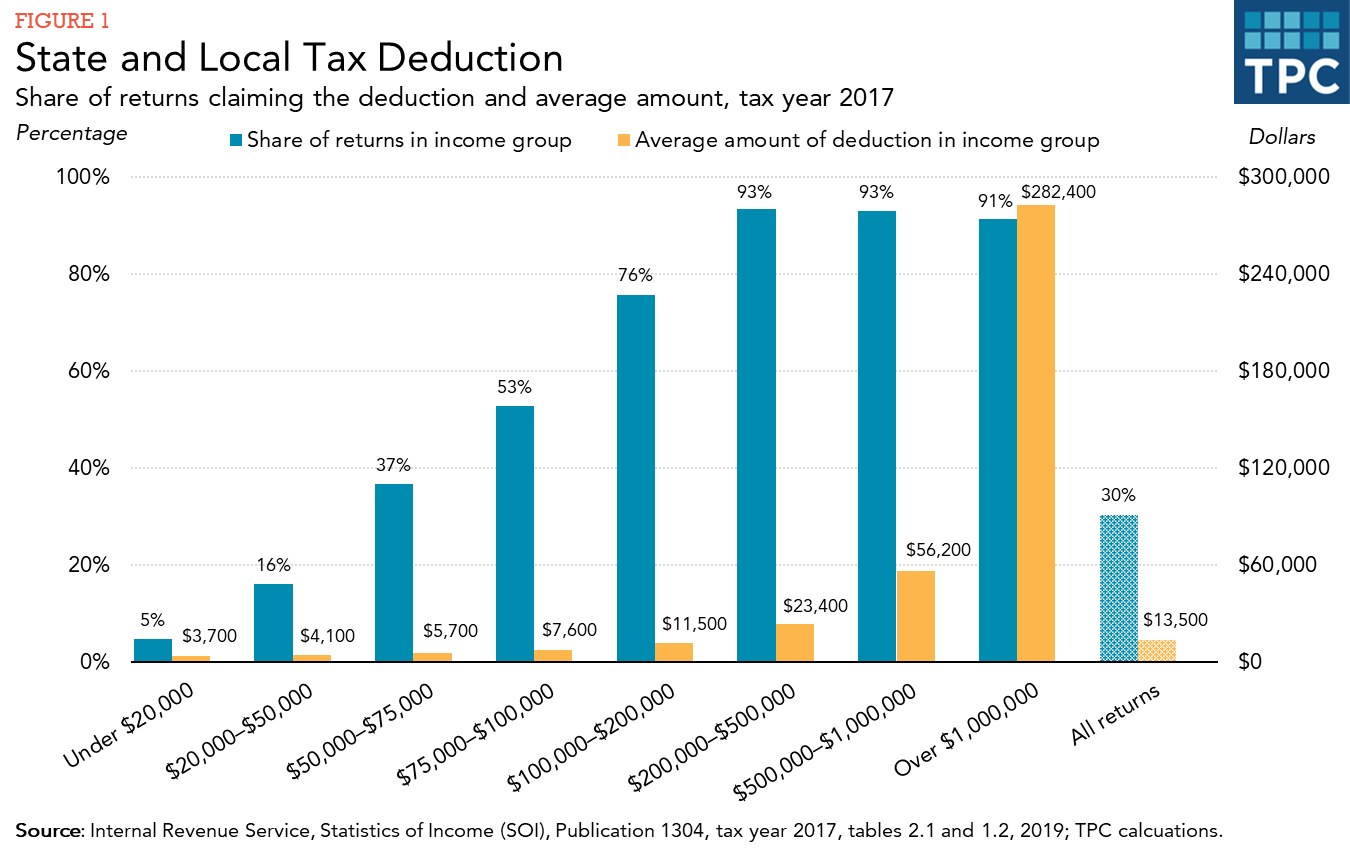

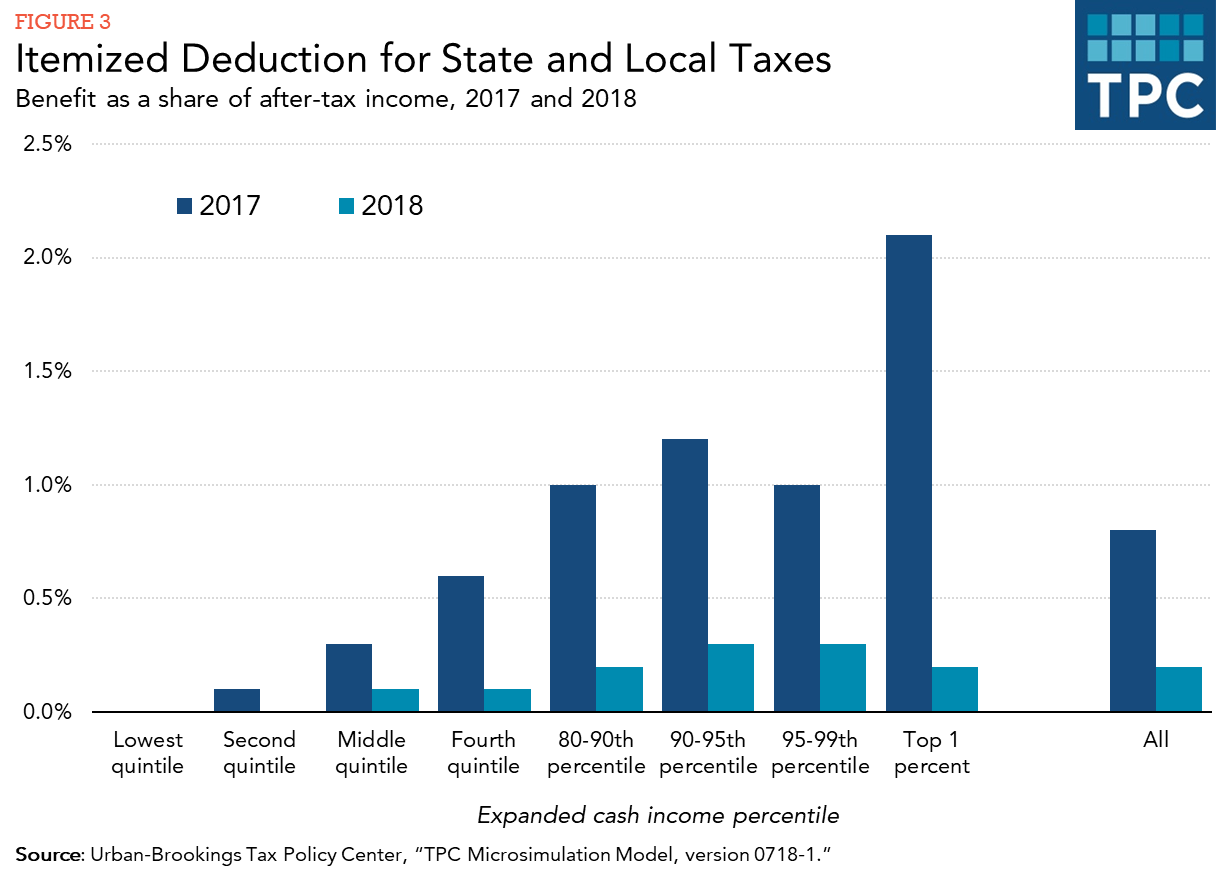

How Does The Deduction For State And Local Taxes Work Tax Policy Center

W4 Exemption In Taxes Tax Tax Preparation Tax Season

Pin On Drk Muse Collective

How Does The Deduction For State And Local Taxes Work Tax Policy Center

Income Tax Rule Change Tripple Tax Benefits On Nps Know How It Works Who Can Claim In 2022 Income Tax Return Income Tax Tax Rules

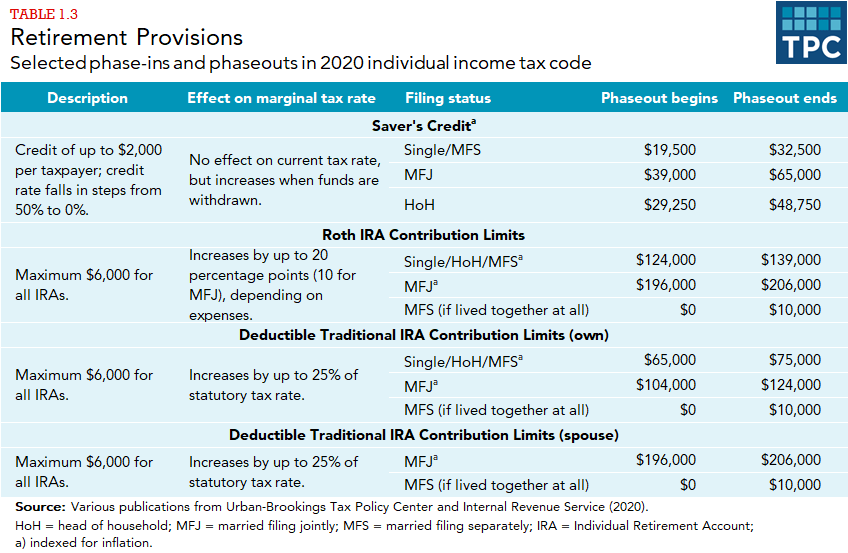

How Do Phaseouts Of Tax Provisions Affect Taxpayers Tax Policy Center

Know More About Itr Form 2 At Taxraahi Taxraahi Is Your Online Tax Return Filing Companion In Delhi Gurgaon Noida An Income Tax Return Tax Return Income Tax

How Does The Deduction For State And Local Taxes Work Tax Policy Center

Introduction To Investing Power Point Presentation 1 12 1 G1 Investing Investment Tools Certificate Of Deposit